Steiner and Company produces the Profit Maximizer report on behalf of National Pork Board based on information we believe is accurate and reliable. However neither NPB nor Steiner and Company warrants or guarantees the accuracy of or accepts any liability for the data, opinions or recommendations expressed.

Highlights

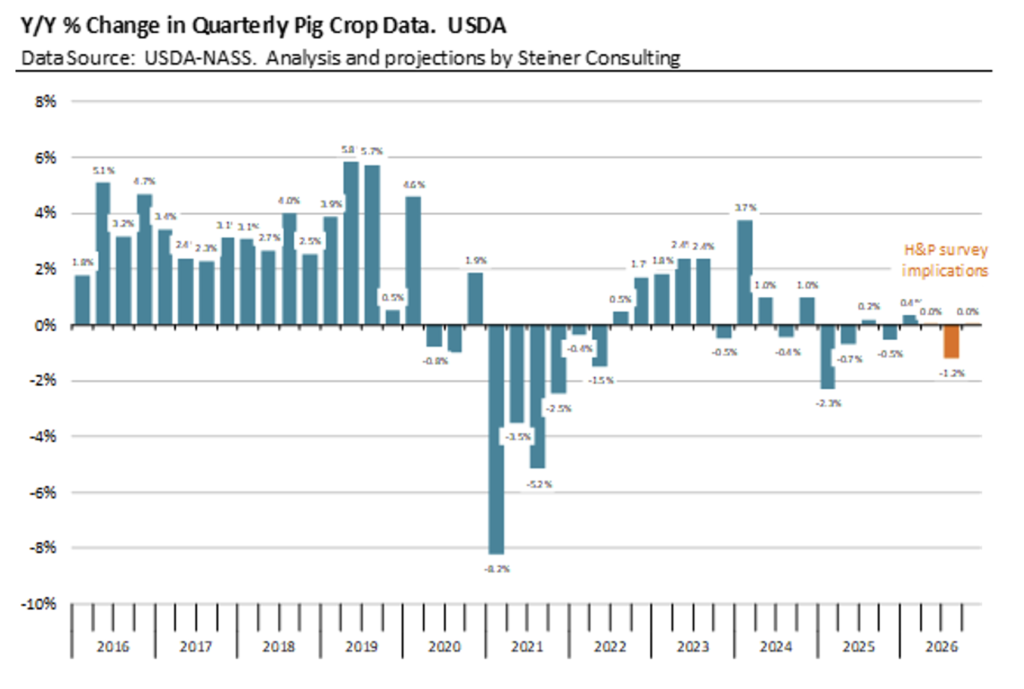

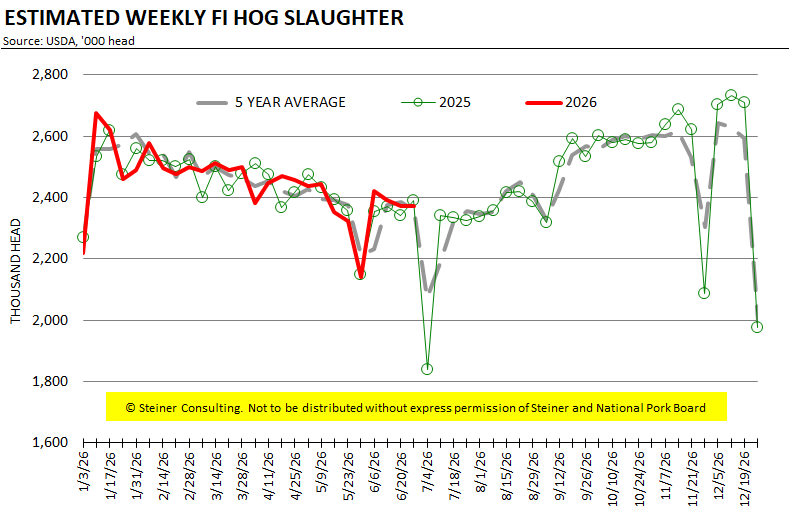

- Limited supply growth in second half of the year: Nearly every inventory category came in at or below expectations, indicating pork production in the second half of the year may increase less than previously thought. USDA in June estimated second half pork production to be up 1.9%, possible but will rely more on continued gains in hog carcass weights.

- Fall slaughter outlook: Lower inventories of 50-119 lb hogs and a flat March-May pig crop suggest fall slaughter will remain close to last year’s levels rather than the 1.5% increase expected from previous reports.

- Demand remains the key challenge: Weak wholesale demand, particularly for processing items, continues to pressure hog and pork prices. However, tighter supplies should help limit downside price risk if inventories normalize and seasonal fall demand improves.

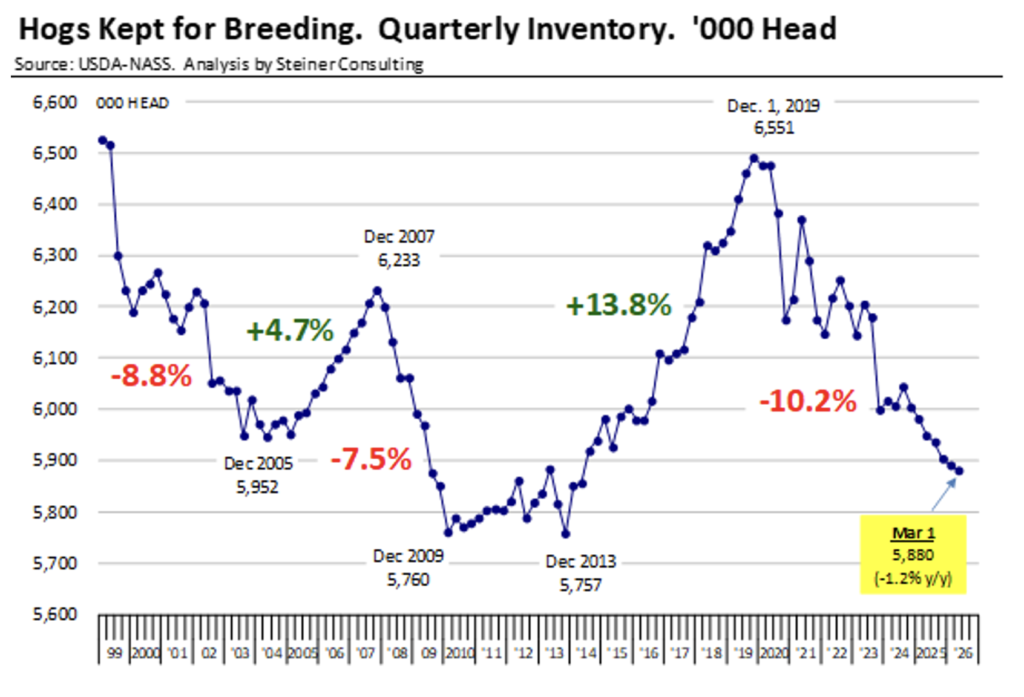

- Smaller breeding herd raises 2027 supply risk: The breeding herd fell 1.2% y/yr to its smallest June 1 level since 2014, limiting production growth potential and increasing the industry’s vulnerability to disease outbreaks or higher feed costs.

Full Report

Decline in Hog Breeding Herd Will Continue to Impact Growth Potential, Heighten Disease/Feed Cost Risks for 2027

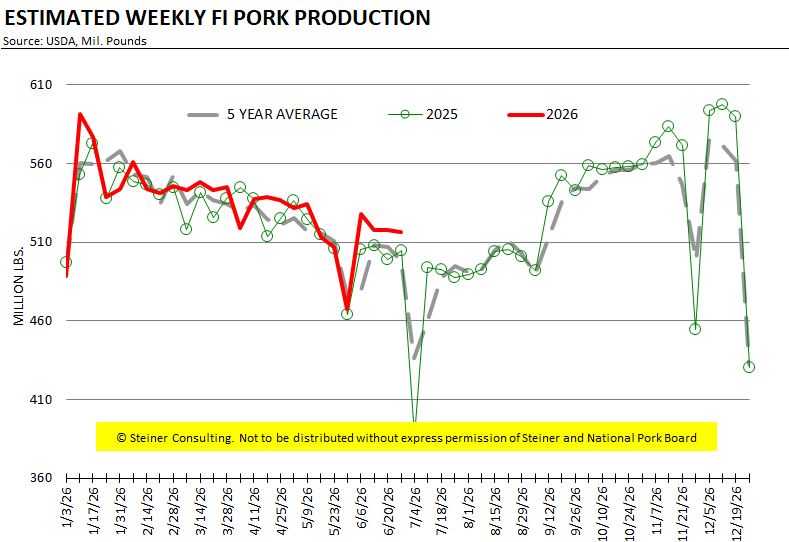

USDA’s June Hogs and Pigs report pointed to a tighter supply outlook than analysts were expecting coming into the survey. Nearly every major inventory category came in at or below the low end of pre-report estimates, suggesting that pork production during the second half of the year may not expand as much as previously expected. While the report is supportive from a supply perspective, it should be noted that the market’s biggest challenge today is demand, not supply. Indeed, the ongoing weakness in wholesale demand, especially for processing items, has resulted in a sharp repricing of hog/pork prices this summer and out front. Note that we say wholesale rather than consumer demand. That’s because we think the current weakness is in part the result of processors and end users overestimating consumer demand and seeking to anticipate product inflation by building inventories for the spring and summer.

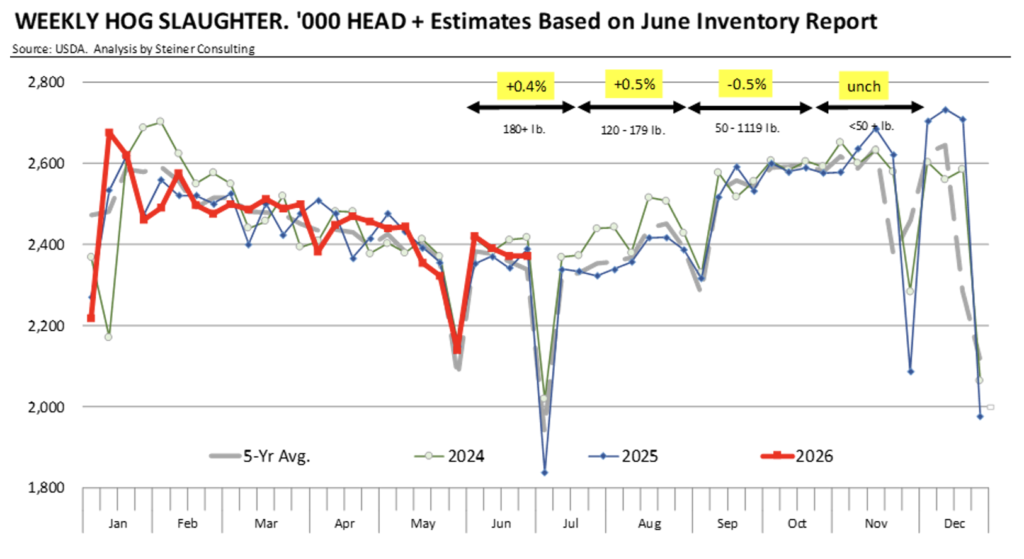

The breakdown of the market hog inventory suggests only modest growth in slaughter during the next several months. The inventory of market-ready hogs over 180 pounds was reported only 0.4% above last year. Actual June slaughter has been stronger than those inventories would imply, leaving some question about whether the survey understated near-term supplies. If USDA’s numbers prove accurate, slaughter after the holiday will remain limited and well below the 2.4 million level we saw in late May and June.

Inventories of hogs weighing 120-179 pounds, which largely determine marketings during July and first half of August, were also lower than expected. More notable was the inventory of 50-119 pound hogs, which was reported 0.5% below a year ago after the market had anticipated an increase. Those hogs largely determine slaughter during late August through mid-October and suggest that fall production may be somewhat smaller than previously projected. Under-50 pound inventories were unchanged from a year ago, implying that slaughter during late October and November should remain manageable from a processing standpoint, although supplies will still seasonally increase.

More About Fall Supply Expectations

The March-May pig crop provides another indication that fall supplies may not expand significantly. USDA estimated the pig crop at essentially unchanged from last year compared to trade expectations for roughly a 1.3% increase. If realized, this would point to slaughter during much of the fourth quarter remaining close to last year’s levels rather than any significant y/y growth. Current futures prices already reflect considerably weaker demand than last year, with October and December contracts trading well below where they settled in 2025. While demand remains the larger source of uncertainty, the latest supply estimates should help limit downside price risk if wholesale demand stabilizes. This could come from processors finally drawing down inventories as well as low prices encouraging more retail and foodservice features/promotions in the fall. October is pork month and generally sees good pork demand.

Breeding Herd Signals Limited Supply Growth in 2027

While quarterly farrowing intentions often receive considerable attention, we have always thought that the breeding herd provides a better indication of longer-term production potential. USDA estimated the June 1 breeding herd at 5.88 million head, down 1.2% from a year ago and below what most analysts expected prior to the report. The smaller breeding herd indicates that producers continue to expand cautiously despite improved profitability compared to the last several years.

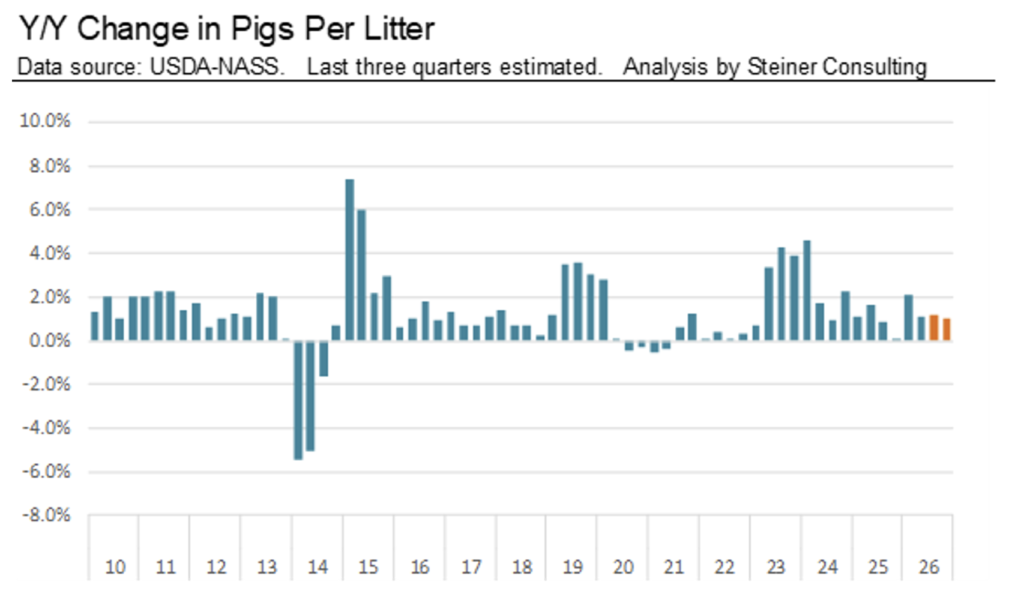

Without a meaningful increase in breeding inventory, future pork production will continue to depend primarily on productivity gains rather than herd expansion. Improvements in pigs saved per litter have remained remarkably consistent and should continue to support modest production growth. However, those gains alone are unlikely to result in any significant increases in pork supplies without additional gilt retention.

The smaller sow herd also highlights the industry’s continued exposure to disease risk. Producers have become increasingly cautious about expansion due to uncertain domestic and export demand. As a result, much of the supply growth has come from productivity gains, be this more pigs per litter, higher farrowing rate or heavier hogs. Disease outbreaks could significantly impact overall productivity, especially summer supply that seasonally declines in even the best year. While summer prices this year are lower than expected, we still think it is important to have a consistent risk management program for the Jun-Aug period, especially as pork producers now rely on the smallest breeding herd since 2014.

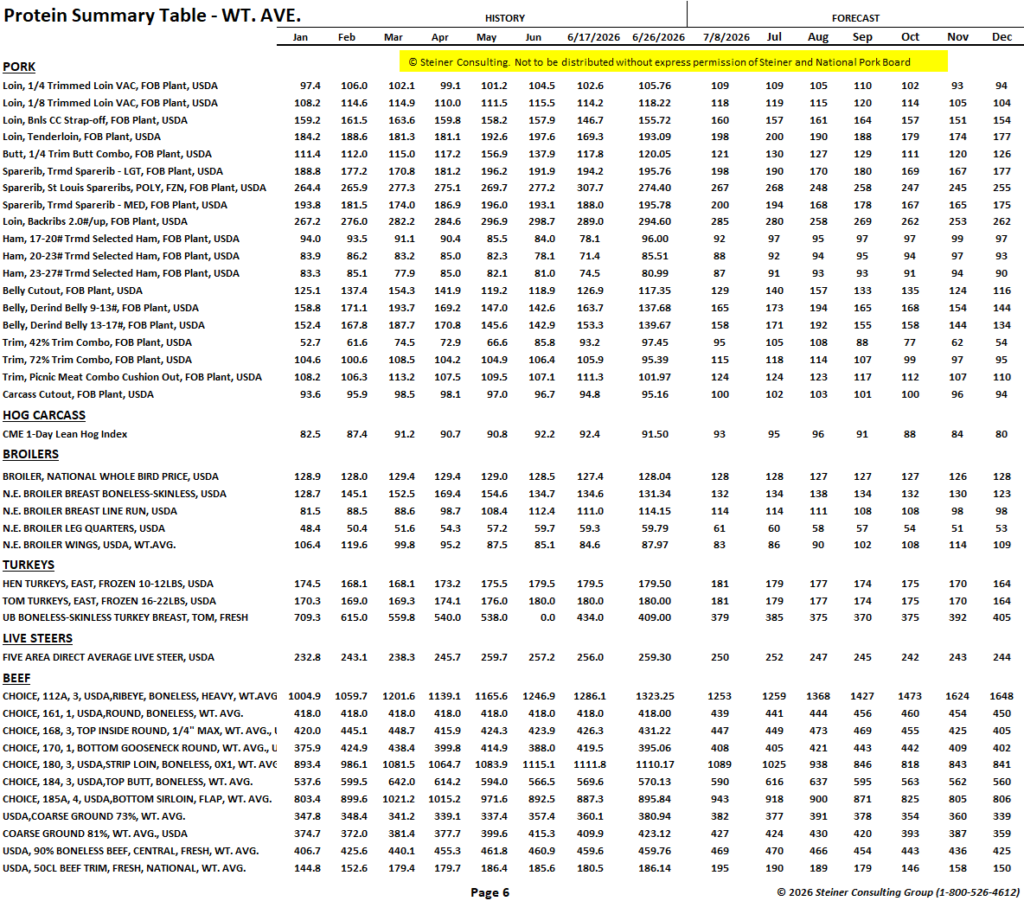

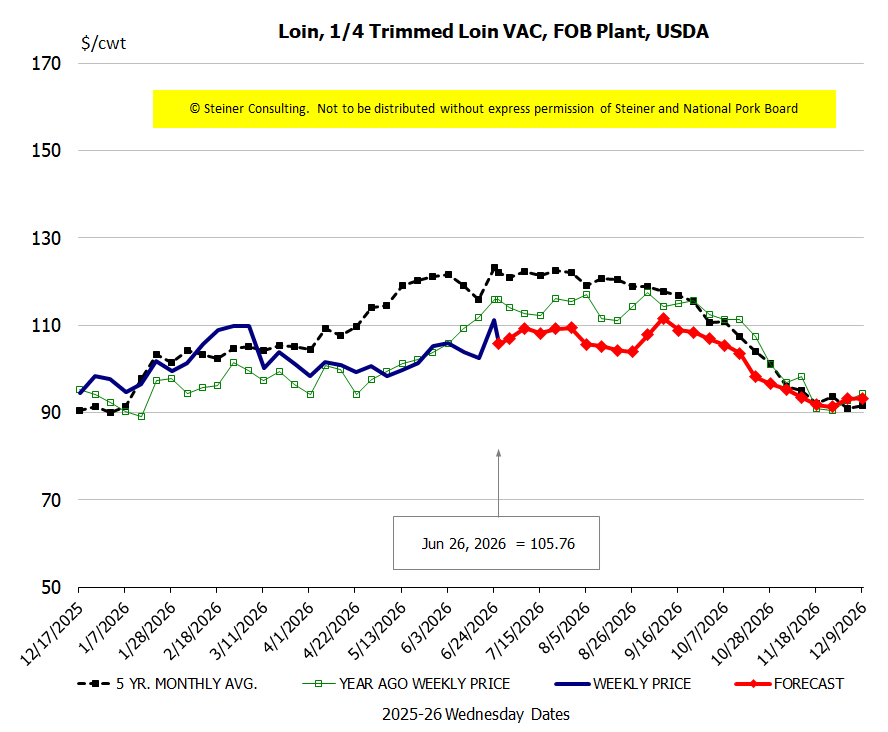

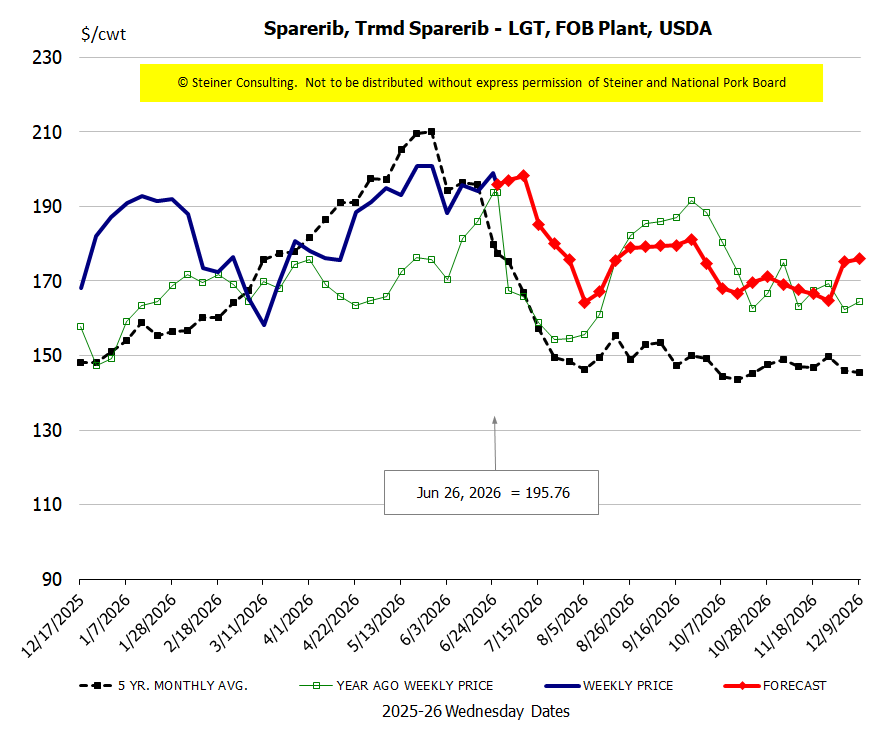

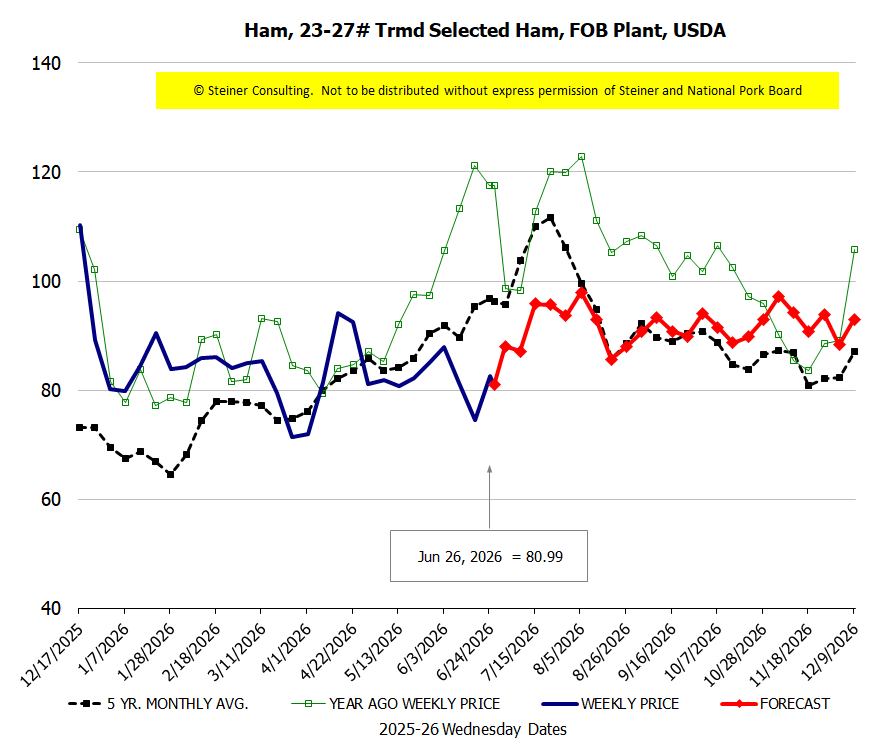

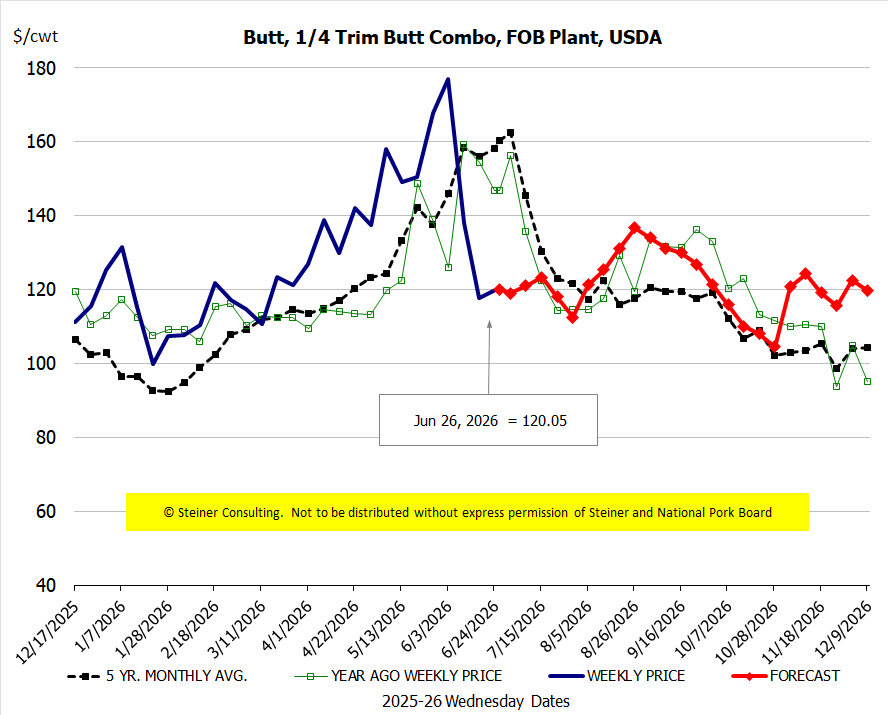

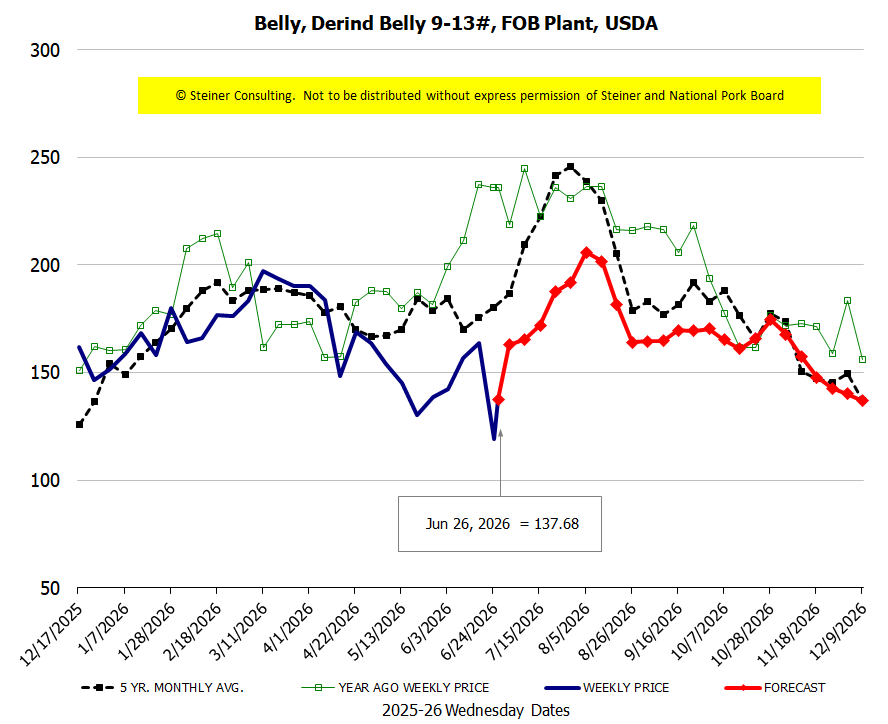

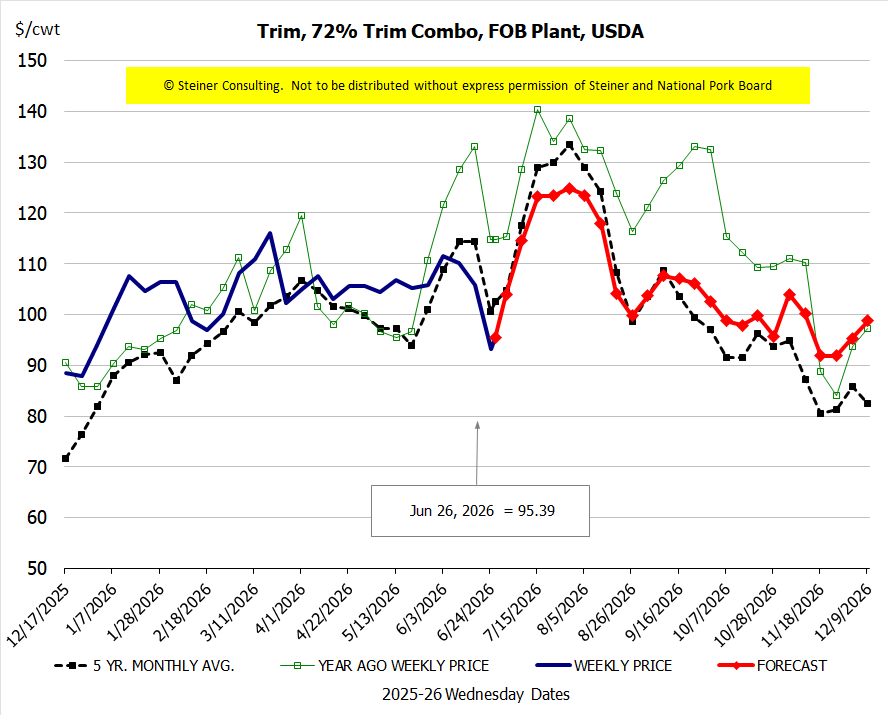

Price Chart

Forecasts

Steiner Consulting Group produces the National Pork Board newsletter based on information we believe is accurate and reliable. However, neither NPB nor Steiner and Company warrants or guarantees the accuracy of or accepts any liability for the data, opinions or recommendations expressed.